Customer Master Data, a Strategic Asset for Financial Institutions Navigating AML, KYC, Risk, and Portfolio Complexities

The financial sector, banks, lenders, wealth advisors, mortgage brokers, and firms dealing with diverse financial instruments, operates under immense burdens of regulatory scrutiny and customer expectation.

The critical pillars of Anti-Money Laundering (AML), Know Your Customer (KYC), comprehensive Risk Management, and meticulous Portfolio Administration all hinge on one fundamental asset: accurate, accessible, and well-governed customer data.

The Pretectum Customer MDM solution, offers a robust, flexible SaaS platform poised to deliver substantial benefits across these crucial domains by transforming how financial institutions manage their people-based master data.

Stronger AML and KYC Compliance through Unified Customer Views

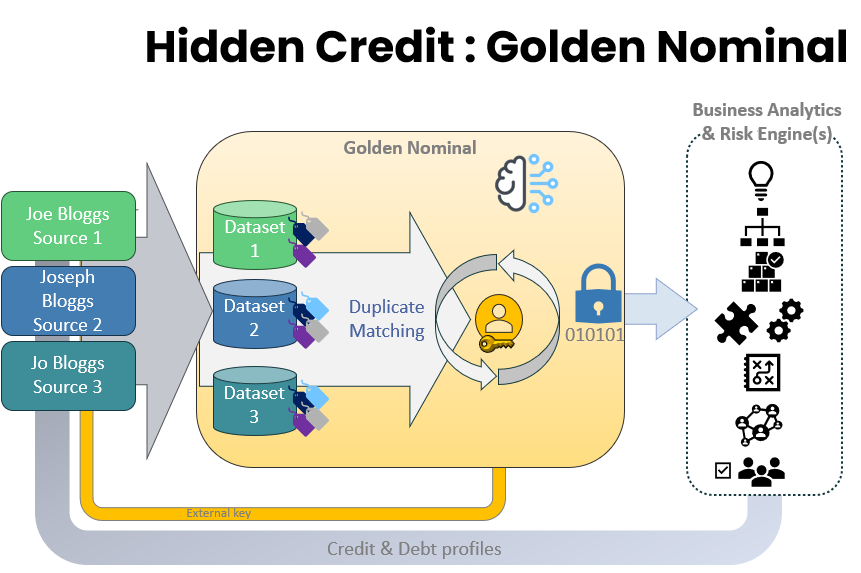

The cornerstone of effective AML and KYC programs, is the ability to uniquely identify and understand each customer – the elusive “Golden Record.” Pretectum’s architecture is fundamentally designed to achieve this.

Breaking Down Silos: Financial institutions often suffer from fragmented customer data spread across disparate systems (core banking, loan origination, wealth management platforms, trading systems). Pretectum data partitioning by business area allows for organized data management, while its ability to define multiple data models enables the ingestion of data from these diverse sources – be it via CSV imports, JDBC connections, REST APIs, or streaming.

Building the Golden Record: The platform’s duplicate matching process is paramount. By matching records across business areas and datasets using tags and underlying data values, it identifies potential duplicates. The subsequent merge/purge process, guided by configurable survivorship rules, consolidates these into a single, reliable master record for each individual. This unified view is crucial for AML checks, ensuring that all accounts and activities related to a single individual are considered, reducing the risk of overlooking suspicious patterns distributed across siloed views.

Enhancing Data Quality for Screening: Strong data typing, validation rules, and the use of business area data (e.g., ISO country codes for jurisdiction risk, honorifics for identification) ensure that incoming data is standardized and accurate. This dramatically improves the efficiency of screening processes against sanctions lists, Politically Exposed Persons (PEP) lists, and other watchlists, minimizing false positives and focusing investigative resources.

Dynamic Data and Consent: Self-service data validation and consent granting feature is particularly relevant. It not only empowers customers but also ensures data is up-to-date directly from the source. For KYC, obtaining explicit consent for data processing, with an auditable record, is increasingly vital.

This feature also allows individuals to review and correct their information, maintaining KYC data integrity over time.

Elevating Risk Management Capabilities

Accurate customer data is the bedrock of sound risk management, whether it’s credit risk, operational risk, or compliance risk.

- Comprehensive Customer Risk Profiling: A unified customer view, enriched with accurate attributes, allows for more precise risk scoring and segmentation. For lenders and mortgage providers, understanding a customer’s full financial picture, potentially consolidated through Pretectum, leads to better credit decisions.

- PII Protection and Access Control: The financial industry handles vast amounts of Personally Identifiable Information (PII). Pretectum’s automatic PII masking upon ingestion, coupled with role-based access controls (RBAC) and the requirement for re-authentication to unmask PII, significantly strengthens data security. This granular control, logged in an audit trail, is crucial for meeting data privacy regulations (like GDPR) and mitigating internal fraud risks. This secure handling of data reduces the risk of data breaches, which carry severe financial and reputational consequences.

- Streamlined Auditing and Reporting: The comprehensive audit logs tracking data changes, access, consent events, and PII unmasking provide an invaluable resource for internal audits and regulatory reporting, demonstrating due diligence and compliance.

- Flexible Data Scope for Holistic Risk Views: The ability to ingest various data types, including potentially transactional data alongside master data, can offer deeper insights for risk modeling, although the primary intent is people master data. Understanding transaction patterns in conjunction with a verified customer identity is a powerful tool for fraud detection and AML.

Optimizing Portfolio Administration and Client Advisory

For wealth advisors and brokerage firms, maintaining accurate client data and providing personalized service is key to success and regulatory compliance.

- Accurate Client Records: The “Golden Record” established by Pretectum ensures that advisors have the correct contact details, financial standing (as per consolidated data), and communication preferences for their clients. This is vital for distributing statements, trade confirmations, market updates, and fulfilling suitability requirements.

- Efficient Client Onboarding and Maintenance: The ability to manually add records with real-time validation or import data with lightweight ETL transformations streamlines the onboarding process. The self-service portal can also be used to periodically refresh client information, ensuring ongoing accuracy.

- Targeted Communication and Service: The flexible data tagging functionality, which doubles as a business glossary (potentially using AI prompts for focused tag creation), allows for sophisticated client segmentation. Advisors can classify clients based on investment profiles, risk appetite, or other relevant attributes, enabling more targeted advice and service offerings.

- Enhanced Search and Discovery: The AI-powered elastic search using natural language queries is a game-changer. Portfolio administrators or compliance officers can quickly find specific client records or groups of records based on complex criteria without needing to understand intricate database query languages. This is invaluable for responding to client inquiries, internal investigations, or regulatory requests efficiently. For instance, finding all clients holding a specific financial instrument or residing in a particular jurisdiction becomes a simple task.

The Overarching Benefit: A Foundation of Trust and Efficiency

The Pretectum Customer MDM solution offers financial institutions a pathway to move beyond reactive data cleanup to proactive data governance. By establishing a trusted, unified view of each customer, the platform enables:

- Reduced Compliance Costs: Streamlined AML/KYC processes, fewer false positives, and easier auditability translate to lower operational costs associated with compliance.

- Minimized Risk Exposure: Better data quality and comprehensive customer views lead to more accurate risk assessments and a stronger stance against financial crime.

- Improved Operational Efficiency: Automation of data ingestion, validation, matching, and the intuitive AI search free up valuable human resources from manual data wrangling, allowing them to focus on higher-value activities.

- Enhanced Customer Experience: Accurate data and self-service options lead to smoother interactions, personalized service, and increased client trust.

- Greater Agility: The platform’s flexibility in defining data models and integrating with diverse sources allows financial institutions to adapt more quickly to new regulations, products, or business structures.

For any entity in the financial sector grappling with the intricacies of AML, KYC, risk management, and portfolio administration, a solution like Pretectum is not merely a technological upgrade or tool for digital transformation, but a strategic advantage.

Providing foundational data integrity and accessibility in alignment with the needs of modern banking, it enables adopters to navigate the growing complexity of regulatory frameworks, manage risks more effectively, and ultimately, build more resilient and customer-centric financial operations.

The ability to harness clean, reliable, and interconnected customer data is the key to unlocking significant competitive advantages and ensuring long-term stability in an ever-evolving industry. Contact us to learn more about how Pretectum CMDM can help #LoyaltyIsUpForGrabs