Pretectum’s Customer Master Data Management (CMDM) platform can play a pivotal role in identifying and mitigating the risks associated with “hidden credit” practices, where individuals maintain undisclosed financial obligations.

By consolidating customer data from various sources into a centralized repository, Pretectum CMDM creates a comprehensive view of customer interactions, behaviors, and financial profiles, which is essential for detecting inconsistencies or discrepancies that may indicate hidden credit activities.

The platform’s robust data governance features ensure high data quality and accuracy, allowing organizations to implement effective monitoring and auditing processes that can flag potential financial infidelity.

Additionally, real-time data processing capabilities enable businesses to support adaptive risk management strategies promptly, based on the latest customer interactions.

When integrated with reporting and analytics tools, Pretectum CMDM offers up markers and traits in customer profiles that are tied into customer behavior patterns, empowering organizations to make informed decisions and proactively address potential risks associated with undisclosed credit accounts.

Overall, Pretectum CMDM enhances transparency and accountability in customer data management, which is crucial for reducing lender risk and fostering trust in financial relationships.

Hidden Credit’s Key Characteristics

“Hidden credit” typically refers to financial practices where individuals maintain undisclosed credit accounts, debts, or financial obligations, often leading to situations of financial infidelity or deception.

Hidden Credit can include secret credit cards, BNPL liabilities or loans that are not disclosed to those they transact with, which can create significant trust issues and financial complications.

The concept is often associated with behaviors aimed at making use of credit beyond the affordability of the individual, and such practices can lead to increased debt levels and risk for lenders and those providing sales credit or debt.

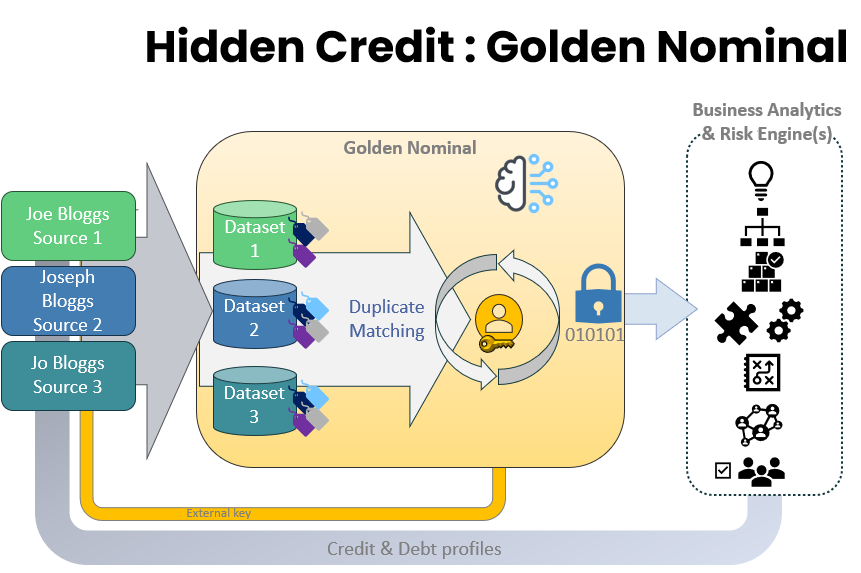

Hidden debt may be present within one’s own portfolio of customers, but it can also be visible through the consolidation of data from multiple sources. Focusing on one’s own book of customers, an organization would need to be able to identify where the same person is present multiple times in the customer system but under slightly different profiles.

Identifying these individuals and consolidating their risk profile presents a better picture to an organization that wishes to avoid defaults and having to send individuals’ debt and liabilities for collection.

Financial Services: A customer may have multiple accounts with different banks, using variations of their name or address. An external key, such as a national identification number or social security number, can help link these accounts, revealing the true financial status and credit obligations of the individual but in the absence of these some other external key such as that from Pretectum CMDM would assist.

Insurance Policies and Claims: An individual might submit claims to different insurance providers under slightly different names or addresses to hide a history of claims. By tying an individual to a unique identifier such as that found in the Pretectum CMDM, insurers can consolidate these claims and assess the risk more accurately, preventing fraudulent activities.

E-commerce Platforms: A shopper might create multiple accounts on an e-commerce site using different email addresses or names to exploit discounts or promotional offers. An external key from a Golden Nominal repository like that of Pretectum CMDM, linked to their payment information can help identify these accounts as belonging to the same person, enabling the platform to enforce fair use policies.

Healthcare Records: Patients may provide inconsistent personal information across various healthcare providers. By utilizing a unique patient identifier, healthcare systems can merge records from different providers, ensuring accurate medical histories and improving patient care; this same approach minimizes the likelihood of patient pharma abuse. Pretectum CMDM can provide an external key based on common traits across the patients to find a common thread that identifies the many apparent patients as one and the same person.

Telecommunications: A customer may open multiple phone lines under different names to evade payment obligations. An external key linked to billing information can help telecom companies identify these accounts as belonging to the same individual, reducing financial risk.

Real Estate: A tenant may open rent multiple properties under different names to evade payment obligations or to facilitate subletting. An external key linked to billing information can help property management companies to identify these accounts as belonging to the same individual, reducing their financial risk and exposure and neutralizing unauthorised subletting.

Utilities: An applicant may open accounts for different properties, under different names to evade payment obligations or to circumvent certain account profiling types. An external key linked to billing information can help utility companies to identify these accounts as belonging to the same individual, reducing their financial risk and exposure.

Line of Credit or Loan Applications: Individuals may attempt to apply for multiple lines of credit or loans under slightly different names ahead of the credit verification process. By cross-referencing applications with an external key, lenders can identify overlapping applications being made concurrently .

Social Media Accounts: Users might create multiple profiles on social media platforms with slight variations in their names or birthdates to manipulate engagement metrics or avoid bans. An external key based on device identifiers or IP addresses can help platforms detect and merge these duplicate accounts.

Credit Reporting Agencies: Individuals may attempt to hide debts by using different names when applying for credit. By cross-referencing applications with an external key such as a tax identification number, agencies can identify overlapping financial obligations and assess creditworthiness more accurately.

In each of these scenarios, the use of an external key from a golden nominal is crucial for linking disparate pieces of information and revealing the true identity of individuals who may be trying to obscure their financial obligations or personal details across various systems.

Pretectum CMDM’s value in reducing risk

Pretectum’s Customer Master Data Management (CMDM) platform is particularly useful in addressing the risks associated with “hidden credit” practices by providing a centralized, unified and comprehensive view of customer data, essential for identifying potentially duplicative customer profiles and in turn, undisclosed financial obligations.

By consolidating data from multiple sources, Pretectum CMDM creates a single source of truth about customers, that enables organizations to detect potential inconsistencies or discrepancies in customer profiles, such as multiple accounts under different identities but with common attributes, such as phone numbers or email addresses or addresses.

The platform’s robust data governance features ensures high data quality and accuracy, which maintaining privacy, facilitating effective monitoring and auditing processes that can flag potentially problematic customer profiles and ultimately, the potential for financial infidelity yet remain within the boundaries of privacy and data protection regulations.

Real-time data processing capabilities allow businesses to adapt their risk management strategies promptly based on the latest customer interactions, while integration with reporting and analytics tools can help when leveraging identifier markers and traits linked to risky financial behaviors.

The holistic approach to customer master data management in general, enhances transparency and accountability in customer data management, ultimately reducing lender and credit sales risk and fostering trust in financial relationships by proactively addressing potential risks associated with hidden credit.

Use Cases

Customer Identity Verification: Banks can utilize CMDM to verify customer identities across multiple accounts, reducing the risk of identity theft and fraud. By linking customer profiles through unique identifiers, banks can consolidate data to ensure accurate credit assessments.

Suspicious Activity Monitoring: E-commerce platforms can employ CMDM to monitor transactions for unusual patterns, such as multiple purchases from different accounts linked to the same payment method, which may indicate fraudulent activity.

Application Overlap Detection: Credit card companies can use CMDM to identify applicants who submit multiple applications under different names or addresses, helping to prevent fraudulent approvals and manage credit risk more effectively.

Account Consolidation: Telecom providers can leverage CMDM to consolidate customer accounts that may have been created under different names or addresses, thus preventing abuse of services and ensuring accurate billing.

Risk Assessment: Insurers can utilize CMDM to assess risk more accurately by consolidating claims data from various policies held by the same individual, thereby reducing the likelihood of fraudulent claims.

Patient Record Consolidation: Healthcare providers can use CMDM to merge patient records from different facilities, ensuring comprehensive medical histories and minimizing the risk of fraudulent claims or prescription abuse.

Welfare Fraud Detection: Government agencies can implement CMDM to detect individuals who may be receiving benefits under multiple identities, thereby ensuring that resources are allocated fairly and reducing fraud.

Account Duplication Prevention: Retailers can use CMDM to identify customers who create multiple loyalty program accounts to exploit rewards, allowing them to enforce fair usage policies and enhance customer loyalty management.

Tenant Screening: Property managers can utilize CMDM to screen prospective tenants by consolidating rental applications and payment histories, helping to identify individuals who may have a history of evading rental obligations.

Risk Profiling: Peer-to-peer lending platforms can leverage CMDM to assess borrower risk by consolidating financial profiles across different platforms, ensuring a comprehensive view of an individual’s creditworthiness.

Pretectum’s CMDM platform capabilities hold value in various sectors by providing a unified view of customer data that can enhance risk management practices. Its capabilities in identifying hidden credit activities through data consolidation and real-time processing could make it a valuable tool for organizations aiming to mitigate financial risks and foster trust in their customer relationships.